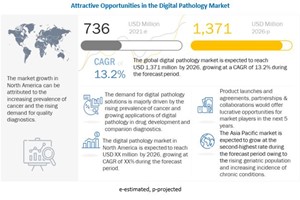

The global digital pathology market is valued at an estimated USD 736 million in 2021 and is projected to reach USD 1,371 million by 2026, at a CAGR of 13.2% during the forecast period. The growth in the digital pathology market is mainly driven by factors such as the increasing adoption of digital pathology to enhance lab efficiency, rising incidence of cancer, and growing applications of digital pathology in drug development and companion diagnostics.

Covid-19 Impact on the Digital Pathology Market

Amidst the growing number of cases and deaths due to COVID-19, various solution providers are collaborating with healthcare institutions, like hospital laboratories and other laboratory facilities, to deal with the increasing number of tests coming to laboratories for COVID-19 screening and diagnosis.

Regulatory authorities like the FDA are relaxing their regulations temporarily to encourage the use of digital pathology solutions. For instance, the agency decided to relax its regulation in the last week of March to reduce the immediate risk of the virus to pathologists. The agency does not intend to object to modifications to already cleared digital pathology devices to allow for remote use or the marketing of new remote digital pathology devices without submitting a 510(k), so long as the devices do not create undue risk. For instance, Leica Biosystems received notification from the US FDA in 2020 to exercise enforcement discretion for using Aperio WebViewer for remote diagnosis with the help of images obtained from Aperio AT2 or Aperio AT2 DX digital pathology scanners during the COVID-19 emergency. Philips also received notification from the US FDA to exercise enforcement discretion for using Philips IntelliSite Pathology Solution for pathologists who can review pathological cases remotely during the COVID-19 emergency.

With the COVID-19 pandemic, most countries, including Europe, the US, India, and Australia, followed a complete lockdown. This lockdown and restrictions related to social distancing led to an increase in the use of digital pathology solutions that help in remote access to diagnostic tests performed in CLIA-certified laboratories. The sales of digital pathology scanners and storages decreased in 2019-2020 owing to a lack of interactions required for the demonstration of devices to clients and a lower number of pathological tests conducted in the laboratories. However, the demand for digital pathology solutions has increased after 2020. They help facilitate the continuity of patient care, reduce the risk of healthcare professionals being exposed to coronavirus, and prevent disruption of critical pathology services.

Digital Pathology Market Dynamics

Driver: Increasing adoption of digital pathology to enhance lab efficiency

Digital pathology helps improve lab efficiency by reducing costs, decreasing turnaround times, and providing users with access to subject-matter expertise. Improvements in lab efficiency are critical as patients and physicians are dependent on lab results for diagnostic decisions, and diagnostic tests are required to be completed and reported quickly & accurately. Moreover, access to digital slides via web services eliminate shipping costs and travel time for pathologists. The outbreak of the COVID-19 pandemic has led to the implementation of lockdowns and social distancing restrictions. Such restrictions have increased the demand for digital pathology solutions, as pathologists can use these to view diagnostic results for primary diagnosis remotely.

Restraint: High cost of digital pathology systems

A typical digital pathology system, which includes a slide scanner, an image server, and software, costs around USD 500,000 to USD 700,000. The average price of a digital pathology scanner in the Asia Pacific is around USD 110,000 to USD 130,000. Although large hospitals with significant capital budgets can afford these systems, pathologists and academic institutes with limited budgets or IT support often cannot afford them. Healthcare providers, particularly in developing countries like India, Brazil, and Mexico, have low financial resources to invest in such costly technologies. Moreover, trained staff is required for the efficient handling and maintenance of digital pathology systems. The high cost of these systems, coupled with the challenge of a dearth of skilled personnel to operate digital pathology systems, is expected to limit the adoption of these systems.

Opportunity: Introduction of affordable scanners for private pathology practices

The price point of digital pathology hardware, including scanners, is a major restraint to market growth. Therefore, the development of affordable scanners is expected to offer growth opportunities for players operating in the digital pathology market. Most private medical practices are small businesses and cannot afford expensive digital pathology systems. The introduction of affordable scanners and the propensity of small players to move towards digitization of pathology workflow will encourage its adoption among pathologists with low or limited budgets.

Challenges: Shortage of trained pathologists

Pathologists play a crucial role in performing laboratory tests essential for disease diagnosis. However, there is a gap between the supply and demand of pathologists worldwide, especially in Africa and the Asia Pacific region countries. According to a Springer study (2020), Switzerland's number of inhabitants per pathologist is 35,355; in Canada and the US, this number is 20,658 and 25,325, respectively. In Germany, there is one pathologist per 47,989 inhabitants.

Digital pathology enables medical practitioners to remotely share important information with pathologists beyond geographical boundaries securely and timely. Moreover, advanced technologies, such as AI and machine learning, helps pathologists identify diseases faster and help improve their efficacy and efficiency. Thus, the alarming shortage of pathologists is expected to result in the increased utilization of digital pathology for providing remote pathological consultation and services.

The market in North America is projected to witness the highest growth rate during the forecast period (2021–2026)

North America accounted for the largest share of the digital pathology market in 2020. The increasing prevalence of cancer, rising demand for quality diagnostics, the introduction of favorable reimbursement policies, and the implementation of favorable initiatives by the governments in the US and Canada are major factors driving the growth of the digital pathology market in North America